Interest rates for home buying have fluctuated over time in response to various economic factors, including inflation rates, government policies, and the overall health of the housing market.

Freddie Mac: Freddie Mac publishes a weekly Primary Mortgage Market Survey (PMMS) that provides historical data on mortgage rates dating back several decades. See below for this historical mortgage rate data.

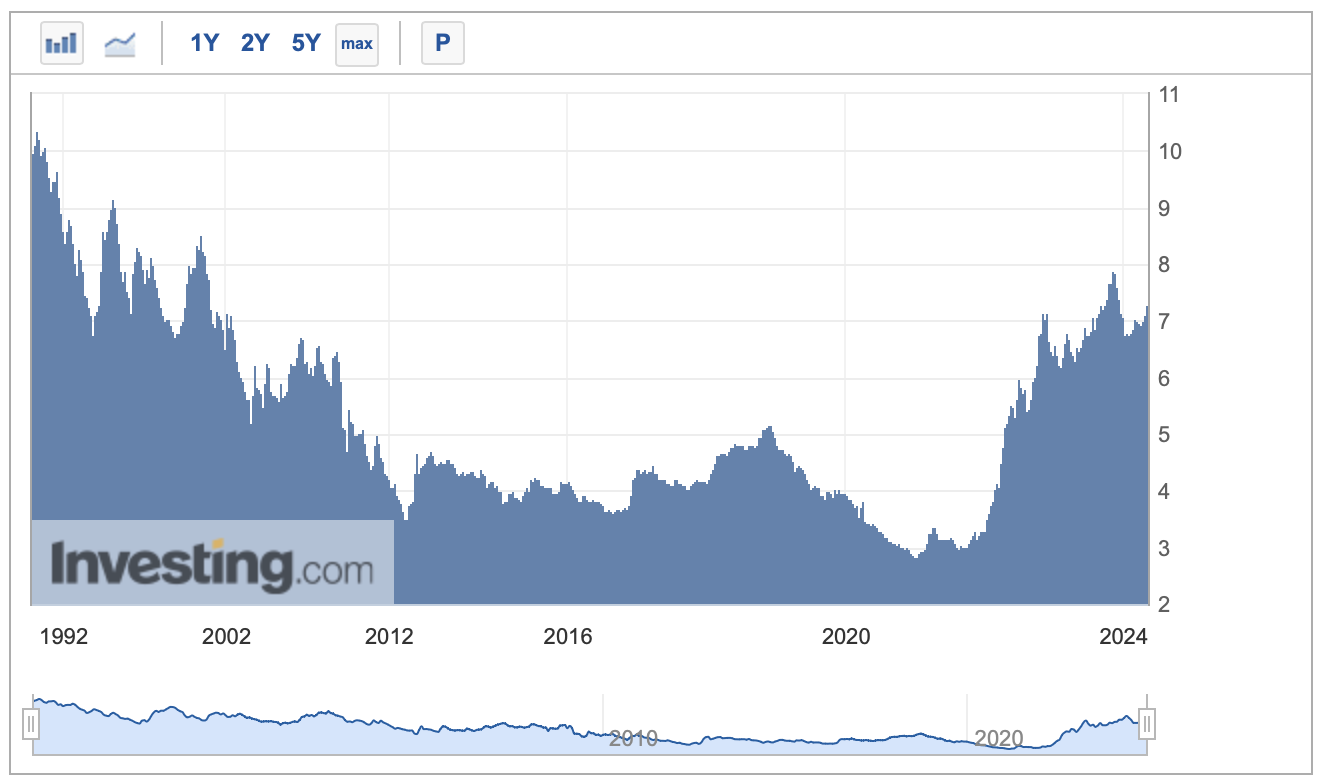

Freddie Mac — the main industry source for mortgage rates — has been keeping records since 1971. Between April 1971 and April 2024, 30-year fixed-rate mortgages averaged 7.74%.

Federal Reserve Economic Data (FRED): FRED, maintained by the Federal Reserve Bank of St. Louis, offers a wide range of economic data, including historical mortgage rates. See below for mortgage rate data from their website.

Investing.com: Investing.com also provides historical mortgage rate data and offers customizable charts that allow you to visualize changes in mortgage rates over time.

Here's an overview of how interest rates for home buying have evolved over the past few decades:

1980s:

- In the early 1980s, interest rates for home mortgages reached historic highs, peaking at around 18-20%.

- This period was characterized by high inflation and tight monetary policy aimed at combating inflationary pressures.

- The Federal Reserve, under Chairman Paul Volcker, implemented aggressive interest rate hikes to bring inflation under control, which led to the spike in mortgage rates.

1990s:

- Throughout the 1990s, interest rates for home mortgages gradually declined from the highs of the 1980s.

- The Federal Reserve, under Chairman Alan Greenspan, pursued a more accommodative monetary policy, which helped to lower interest rates.

- By the late 1990s, mortgage rates had dropped to more moderate levels, making homeownership more affordable for many Americans.

2000s:

- In the early 2000s, mortgage rates remained relatively low, contributing to a boom in the housing market.

- Lenders introduced innovative mortgage products, such as adjustable-rate mortgages (ARMs) and subprime loans, which expanded access to credit but also increased risk in the housing market.

- However, by the mid-2000s, interest rates began to rise gradually as the Federal Reserve sought to curb inflationary pressures and address concerns about asset bubbles in the housing market.

2008 Financial Crisis:

- The housing bubble burst in 2007, leading to a financial crisis that sent shockwaves through the global economy.

- In response, the Federal Reserve slashed interest rates to near-zero levels in an effort to stimulate economic growth and stabilize financial markets.

- Mortgage rates plummeted to historic lows as a result of the Fed's aggressive monetary policy actions.

2010s:

- Throughout the 2010s, interest rates for home mortgages remained at historically low levels.

- The Federal Reserve maintained its accommodative stance on monetary policy to support economic recovery and job creation in the aftermath of the financial crisis.

- Low mortgage rates fueled a resurgence in the housing market, with many homeowners refinancing their mortgages to take advantage of lower interest rates.

2020s:

- In the early 2020s, mortgage rates continued to hover near historic lows amid the economic fallout from the COVID-19 pandemic.

- The Federal Reserve implemented emergency measures, including massive asset purchases and forward guidance on interest rates, to support the economy during the pandemic.

- As the economy began to recover and inflationary pressures intensified, there were expectations for interest rates to gradually rise, although the pace and timing of rate hikes remained uncertain.

Overall, interest rates for home buying have experienced significant fluctuations over time, influenced by a complex interplay of economic factors and policy decisions. While low mortgage rates can make homeownership more affordable, it's essential for prospective homebuyers to consider other factors, such as housing market conditions and personal financial circumstances, when making decisions about purchasing a home. It is also important to note that as mortgage rates drop, more buyers tend to enter the real estate market, and prices trend higher at these times.